A while ago I was at a neighborhood council meeting in Hollywood, and things were getting pretty heated. The topic was the conversion of a rent-controlled apartment building into a boutique hotel, and the people who spoke weren’t shy about saying which side they were on. It was the tenants versus the property owners, and there was no middle ground. Each side was convinced they were absolutely in the right.

The tension was so thick you could cut it with a knife. And it only jacked things up higher when one of the pro-business attendees jumped into the debate. I can’t remember her exact words, but she said something like, “Let’s face it. The vast majority of economists are against rent control.”

I didn’t believe it. I thought she was just trying to bolster her own position. But I didn’t get a chance to call her on it, because the meeting was running late, and ended up lurching to an abrupt halt. The crowd wandered slowly out of the room, with little groups banding together to keep the debate going, while the security guard kept trying to herd us all toward the exit.

Later on, I got on the net to find out what economists really had to say about rent control. And I found out she was right. The vast majority of economists are totally against it. It really floored me when I found a piece Paul Krugman wrote back in 2000 where he argues forcefully that rent control discourages new construction, thereby limiting supply, and inevitably driving rents up. I have a lot of respect for Krugman. I figured if he said it was bad, then it had to be bad.

But the more I thought about it, the more I began to question whether the economists really knew what they were talking about. They’re making the standard argument, that prices rise when supply is short and demand is high, and that prices fall when supply starts to outstrip demand. It’s one of the basics of economic theory, and you can find thousands of examples where the market works exactly that way.

So who am I to tell Paul Krugman he’s wrong? He’s got a Nobel Prize. I don’t even have a college degree. But actually, I don’t think his view lines up with the facts. And here’s why….

In surfing the net, I learned that there are two schools of thought on rent control. The economists who argue that it’s inevitably bad point can point to a mountain of evidence in their favor. But the evidence they’re basing their conclusions on is mostly decades old. In the early- to mid-twentieth century, you had “hard” rent control, which meant setting absolute limits to what landlords could charge for a unit. Once the price was fixed, there was no changing it. The result was poor maintenance, black markets, and little or no construction of new units. But this kind of rent control largely vanished after WWII. And yes, the reason it disappeared in the US was because of a building boom that created huge numbers of houses and apartments, aided by federal policies that made it possible for the average person to get a home loan. Supply-siders please take note. The federal government actively supported middle-income families who wanted to buy a home, spurring the creation of housing developments nationwide.

The second generation of rent control came in the 70s, when rental prices started climbing rapidly. Numerous US cities passed some kind of ordinance to keep a lid on rising rents. And right there the supply siders should see a problem with their argument. If the absence of rent control led to plentiful supply and cheap housing, then nobody would have felt the need to impose regulation. The fact that municipalities all over the US felt pressure from renters to take action indicates that the free market wasn’t working the way it was supposed to.

But the ordinances passed in the 70s were different from “hard” rent control. These measures mostly took a “soft” approach, meaning they didn’t set absolute limits. The Rent Stabilization Ordinance (RSO) passed in LA allowed gradual yearly increases. Also, it only applied to units constructed before 1978. There are economists who are argue that even measures like this still suppress construction, but that didn’t happen in LA. In fact, in the mid-80s the city saw a building boom that created around 100,000 units in the space of a few years. Another feature of “soft” rent control was vacancy decontrol, meaning that when a tenant moved out the landlord could raise the rent as high as they wanted.

But according to the supply siders, it doesn’t matter how you structure it, rent control is bad. And many of them cite LA as a classic example of why it doesn’t work. “Of course tenants are paying outrageous prices there,” they say. “It’s because they’ve got rent control. It drives prices up.” The problem with this argument is that most of the people making it don’t even know which LA they’re talking about. Generally they’re thinking of the County of Los Angeles, not the City of Los Angeles, and there’s a big difference. The County is made up of 88 different cities, and only a few of them have rent control. If the argument put forward by the supply-siders was true, then rents within the City of LA would be higher than rents in surrounding cities that don’t have rent control. But that’s not necessarily the case.

Before I go any further, let me say that finding useful data to make any judgments at all about rent-control isn’t easy. I looked at a number of sources before writing this post, and gradually realized that it’s hard to find reliable, objective info about prices for apartments that are currently on the market. My first move was to look at US Census data, and I quickly ruled it out because it records what tenants are paying instead of prices for units that are currently being offered. That would definitely drive the numbers down in rent-controlled cities, so I had to look elsewhere. I checked out a number of sites that list current rentals, and I was astounded by how high the prices were on some of them. But this is because these sites are mostly geared towards newer apartments, and they often get revenue, directly or indirectly, from the companies that are marketing the units. Another problem is that most commercial sites tend to focus on the hotter markets. Zumper covers the entire US, and regularly issues reports on rental prices. The data they collect is cited by many who write about the market, including journalists. But after taking a closer look I have to question the reliability of Zumper’s info. Check out this map they published this summer about the rental scene in LA.

LA Rental Prices from Zumper, Summer 2016

Based on the data from this sampling, they report that the median rent for a one-bedroom in LA is $1,970, and that LA is the seventh most expensive city in the nation. Let’s take the second claim first. It’s not true. LA may be the seventh most expensive major city in the nation, but there are many cities that are more expensive, including a number in California, like Santa Clara, Redwood City, Dublin, and Cupertino. And none of them have rent control.

Second, this map includes three cities besides the City of Los Angeles. It shows Santa Monica, Beverly Hills, and Culver City. If you think this is nitpicking, let’s move on to the fact that the map actually only shows about half of the City of Los Angeles. It doesn’t include anything east of Downtown or north of the Hollywood Hills. While it includes some neighborhoods where rents are lower, the map seems to have been deliberately drawn to focus on the hottest areas. Why isn’t East LA in the picture? And how come the entire Valley is left out? Is this Zumper’s idea of objective data? There are some pricey neighborhoods in the Valley, but if they’d included Van Nuys, Arleta, Panorama City, Pacoima, Reseda and Sylmar it would almost certainly have brought the median rent for a one-bedroom down. The fact that Zumper’s map is centered on the neighborhoods where prices are highest makes their conclusions seem pretty dubious.

So where do you go to get credible data on current market rates? Honestly, I don’t think there’s any source you can trust completely, but I did find one that seemed more reliable than the others. Rentometer not only covers all of LA, but it also offers information on specific neighborhoods. Its data covers the range of units currently being offered, both new and old. Also, since I wanted to compare LA with other cities that don’t have rent control, I needed a site that would give data limited to a certain area. You may think that’s pretty basic, but I’ve been to sites where I punch in a zip code and they give me everything within a five mile radius.

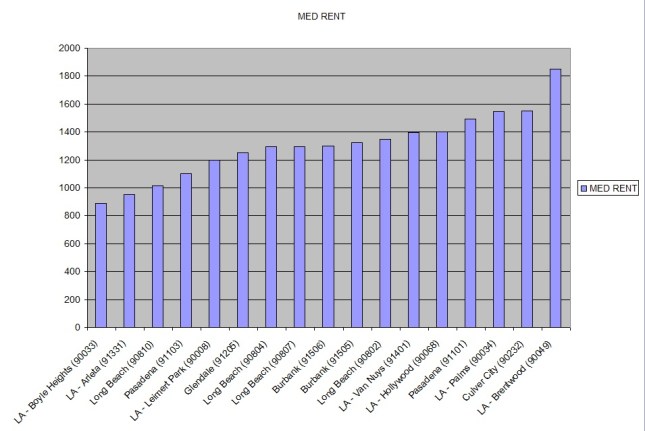

So using Rentometer, I started entering zip codes to compare prices in neighborhoods all over LA County.* Here’s the data I found based on the median rent for a one-bedroom.

LA Rental Prices from Rentometer, Summer 2016

The first thing the graph shows is that there’s a huge range of prices just within the City of LA. This may sound obvious, but again, most commercial sites focus on the high end, and really don’t give an accurate picture of how much variation there is. You can find a huge difference in prices even in neighborhoods that are right next door to each other. I was skeptical about how high the median price given for Van Nuys was, but looking at a map I found that the area covered by this zip code was just west of Valley College. Definitely a more upscale neighborhood than what you’d find around Van Nuys Blvd. and Sherman Way. I was also surprised by how low the median rent was on the west side of Pasadena, but a friend who lives in that city told me that housing around the Foothill Freeway is definitely cheaper.

The second conclusion I came to is that prices don’t seem any lower in cities with no rent control. Neither Burbank nor Long Beach have rent control, but they come out right about in the middle. Pasadena and Culver City don’t have rent control either, and they both appear at the high end. Comparing Palms and Culver City seems like a good way to make my point, since they’re right next to each other. The first is part of the City of LA and subject to rent control, while the second is an independent city where there is no rent control. But the median price for a one-bedroom is almost exactly the same.

I’m sure there are those who will say that this comparison is flawed, since these cities are all within LA County, and that the RSO is causing a spillover effect, pushing up prices even where there’s no rent control. To those people I say, take a look at Orange County. None of the cities within its boundaries have rent control, but you’ll find pretty much the same range of prices.

Is this data conclusive? Or course not. If there’s anybody who can come up with a better source and compile a more comprehensive sample, I’d love to see the results. But based on the data I’ve found, I don’t see any reason to believe that rent control drives prices up. To me it looks like the deciding factor is how desirable an area is for people who have money to spend.

Yes, it’s true that the majority of economists are opposed to rent control. But it’s also true that there’s a younger generation of economists who see the situation as being more complex than your standard supply side formula. I found an article on-line by economist Richard Arnott, (Time for Revisionism on Rent Control?, Journal of Economic Perspectives, Winter 1995) that makes a compelling case for a more nuanced view. Arnott acknowledges that the older “hard” rent control measures were counter-productive, but he doesn’t believe that the newer “soft” measures necessarily have the same damaging impacts.

Arnott also talks about imperfect markets. These are markets where there are forces in play that disrupt the standard dynamic, creating situations that can’t be explained using a simple supply side equation. Twenty first century LA is a great example. Fifty years ago if you built an apartment complex in LA you were most likely marketing your units to people who lived in LA. That’s not true any more. These days developers are pitching their product not just to prospective tenants all over the US, but in some cases all over the world. To them it doesn’t matter if the average Angeleno can’t afford their prices. There’s probably somebody in New York, or Paris, or Seoul, who can.

Here’s something else to consider. With interest rates at record lows, real estate is one of the few sectors that has offered a high rate of return. Investors have been plowing their money into development in search of big payoffs. Why should they waste their time building modest housing for middle-income renters when they could reap huge profits building luxury skyscrapers for the wealthy? This has led to a speculative binge that’s caused real estate prices to skyrocket, and made it difficult for anyone to build housing for middle-income or low-income families. The higher prices charged for new units distort the numbers, and push the so-called “market rate” higher than it should be. A report produced by LA’s Housing + Community Investment Department (HCID) in November 2015 found that there was a 12% vacancy rate in units built since 2005. At the same time, the overall vacancy rate in the city was around 4%. To my mind this shows that these days developers aren’t building units geared toward the people who actually live in LA. If they were, you wouldn’t be seeing such a huge disparity in vacancy rates.

Short-term rentals (STRs) are also having an impact. If landlords find that renters can’t afford their units, no problem. You can actually make just as much money (or more) by listing the units on the net as STRs. Why should a landlord bother with pesky renters who expect a livable dwelling in return for their money, when they can cash in by turning the place into a weekend crash pad? City Hall recently passed legislation to clamp down on this practice, but it’s too early to tell if it’s having any effect.

Again, I’m not going to claim that the data I’ve collected proves anything conclusively, but if anyone wants to argue that rent control is evil, they’ll have to come up with something better. I believe that skyrocketing rents in LA have nothing to do with rent control, and everything to do with a speculative market that’s been actively encouraged by the politicians who run this city. And anyone who wants to make a supply side argument had better show how they’ve factored in the forces described above. When it comes to housing, the landscape has changed. I don’t believe the old rules apply.

If you’re interested in reading more on the subject, I recommend Arnott’s article. Here’s the link.

Time for Revisionism on Rent Control?

*

I should note that when I started checking prices on Rentometer, the site allowed you to search by zip code. That changed recently, and now you have to search by neighborhood. When I looked up the last couple of communities for the graph, I searched by neighborhood and then found the corresponding zip codes.